When you’re closing a limited company, HMRC debt can affect the options available to you. If your company owes VAT, PAYE, Corporation Tax, or other liabilities, HMRC may object to a strike off application and continue recovery action.

The right solution depends on whether the business can repay what’s owed and whether it’s still trading. Where the company cannot pay its debts, a formal closure route such as a Creditors’ Voluntary Liquidation (CVL) is often the most appropriate way to close the company and deal with creditors properly.

At Anderson Brookes, we help directors understand their next steps quickly and clearly, including when strike off is unsuitable and when an insolvency process may be the safer route.

Quick summary: Closing a limited company with HMRC debts

You can’t strike off a company that still owes HMRC – they will object as a creditor

If your company is insolvent, the correct process is a Creditors’ Voluntary Liquidation (CVL)

HMRC is a secondary preferential creditor for PAYE, VAT and similar taxes

Directors can be personally liable if they continue to trade while insolvent or act improperly

A licensed insolvency practitioner ensures the process is legal, compliant, and reduces risk for directors

Table of Contents

Can I close a company with HMRC tax debts?

Yes, you can close a company with outstanding HMRC tax debts, but you must proceed carefully and follow the correct legal process. When your company becomes unable to pay its debts, including tax liabilities to HMRC, it has become insolvent. At this point, your duties as a director change significantly – you must now prioritise the interests of creditors above those of shareholders and directors.

HMRC has considerable powers when it comes to debt recovery and typically acts swiftly against businesses that fail to pay their tax obligations. The tax authority views itself as an “involuntary creditor” since businesses are essentially holding money on HMRC’s behalf through VAT, PAYE and other tax collections. This status gives HMRC stronger enforcement powers than many other creditors.

If you’re considering closing your company with outstanding HMRC liabilities, seeking professional advice from a licensed insolvency practitioner is essential to ensure you follow the correct procedures and protect yourself from personal liability.

Your options for closing a limited company with HMRC debt

There isn’t a single “best” route for every company. The right option depends on whether the business is still viable, whether it can repay HMRC, and whether it is already insolvent.

Here’s a quick comparison of the most common routes.

| Option | When it may be suitable | Key point to know |

|---|---|---|

| Strike off (DS01) | Only where the company has no debts and is not trading | HMRC can object if tax is owed or compliance activity is ongoing |

| Time to Pay (TTP) | The company is viable and can repay over time | Often used to avoid formal insolvency where repayment is realistic |

| Company Voluntary Arrangement (CVA) | The business can trade on and repay creditors over time | A formal agreement with creditors, supervised by an insolvency practitioner |

| Creditors’ Voluntary Liquidation (CVL) | The company cannot pay its debts when due | A formal closure process that deals with creditor claims properly |

| Compulsory liquidation | HMRC or another creditor takes court action | Usually the least controlled route for directors |

If you’re unsure which category you’re in, start with one question: can the company pay its debts as they fall due? If the answer is no, it’s important to take advice early.

Anderson Brookes can help you to close down your limited company with HMRC debts. Call us on 0800 1804 935 or email advice@andersonbrookes.co.uk.

Can you strike off a limited company with HMRC debts?

Many directors mistakenly believe they can simply dissolve their company by submitting a DS01 form to Companies House when they have outstanding HMRC debts. This approach is not legally appropriate and can lead to serious consequences.

A strike-off application is designed for companies that have stopped trading and have no outstanding liabilities. If you apply to dissolve a company while it still owes HMRC, HMRC can object to the strike-off and stop the process. That can leave the company in limbo, with the debt still outstanding and recovery action continuing.

Even if a company is dissolved, it may be possible for a creditor to restore the company to the register in certain situations so that debts can still be pursued. For directors, that can create avoidable stress and additional scrutiny.

If the company owes HMRC and cannot repay, it is usually better to focus on the options that properly address creditor claims.

What happens if HMRC objects to a strike-off?

If HMRC objects, the strike off process can be paused or stopped. That means the company remains active on the register and HMRC can continue to pursue the debt.

Depending on the circumstances, HMRC may also:

- continue standard recovery activity (letters, calls, payment demands)

- pursue enforcement action where they consider it appropriate

- increase pressure if they believe the company is trying to avoid paying what it owes

If the business is genuinely unable to pay, taking the correct closure route typically reduces the risk of a situation escalating unnecessarily.

Alternatives to closing your company

Before proceeding with company closure, it’s worth exploring whether your business might be viable with restructuring. Several options may help you address HMRC outstanding debt while keeping your company operating:

The Time to Pay (TTP) arrangement allows eligible businesses to spread tax payments over an agreed period, typically 3-12 months. HMRC assesses each application individually based on your company’s compliance history and financial projections. You’ll need to demonstrate that your business can afford the proposed repayment schedule through detailed cash flow forecasts and sales projections.

A Company Voluntary Arrangement (CVA) is a formal insolvency procedure that allows your company to repay creditors, including HMRC, over an extended period while continuing to trade. This option requires the approval of 75% of creditors by value but can significantly reduce the monthly payment burden while providing protection from creditor action.

For companies with multiple debts alongside HMRC arrears, business restructuring might be appropriate. This could involve closing unprofitable divisions, renegotiating supplier contracts, or refinancing existing debts to improve cash flow.

However, if these alternatives aren’t viable for your situation, liquidation provides a structured way to close your company and deal with outstanding HMRC debts properly.

Closing a limited company with HMRC debt through a CVL

Where the company cannot pay its debts, a CVL is often the most appropriate way to close the company. It is a formal process that:

- brings trading to an end (unless already ceased)

- appoints a licensed insolvency practitioner as liquidator

- deals with creditor claims fairly and in the proper order

- closes the company once the liquidation is complete

A CVL is not about “walking away” from liabilities. It is a recognised legal route for insolvent companies and is often the clearest way to draw a line under a situation that cannot be rescued.

When a CVL is usually appropriate

A CVL may be the right fit if:

- the company cannot keep up with HMRC payments

- arrears are increasing and there is no realistic way to catch up

- creditor pressure is building

- the company has stopped trading or needs to stop trading

If the company is still viable but needs time, a Time to Pay arrangement or a CVA may be worth exploring instead. The key is matching the solution to the company’s ability to repay.

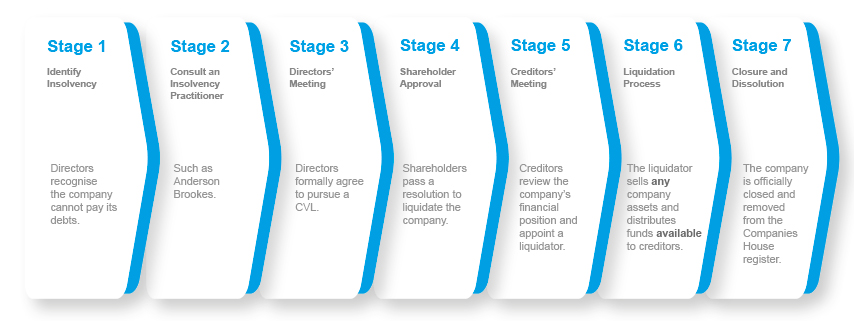

How the CVL process works

Every case is different, but a typical CVL follows a clear sequence:

- Initial review

We gather details on assets, liabilities, and the company’s current position. - Advice on the correct route

We talk through the realistic options and explain the implications for directors. - Decision to proceed

If CVL is appropriate, directors move forward with the formal steps required. - Liquidator appointment

A licensed insolvency practitioner is appointed to act as liquidator. - Notification to creditors

Creditors, including HMRC, are notified and invited to submit claims. - Asset realisation (if applicable)

The liquidator deals with any assets and distributes funds in the correct order. - Company closure

Once the liquidation is completed, the company is closed.

If you want to understand the practical steps involved, we can explain what information we need and how quickly matters can move once a decision is made.

Voluntary Liquidation Process - Quick Example

Need confidential advice about closing your company? Contact us today.

Director responsibilities when closing a company with tax debts

When a company has HMRC debt and is insolvent, directors still have duties and responsibilities. Taking the right steps early can reduce risk and prevent additional problems later.

In most cases this means:

- keeping accurate company records and being ready to share them

- treating creditors fairly

- avoiding decisions that could be viewed as putting one creditor ahead of others

- avoiding asset transfers that don’t reflect fair value

- getting advice as soon as it becomes clear the company cannot pay what it owes

If you are worried about personal risk, the best starting point is a clear assessment of the company’s current position and what options are genuinely available.

HMRC debt management and enforcement powers

HMRC’s debt management department has extensive powers to recover unpaid taxes. These include:

- Taking control of goods through enforcement agents or bailiffs

- Securing debts against company assets

- Imposing personal liability on directors in certain circumstances

- Initiating criminal proceedings for tax evasion

- Petitioning for compulsory liquidation of the company

If your company has fallen behind with tax payments, HMRC will typically begin with reminder letters and escalate to more serious enforcement action if the debt remains unpaid. The full escalation process can move quickly, particularly for VAT and PAYE arrears, which HMRC views as money being held on their behalf rather than genuine company debt.

When a company enters VAT debt management or PAYE arrears, HMRC may initially offer Time to Pay arrangements for businesses they believe are viable. However, if they suspect insolvency or deliberate non-payment, they can move straight to enforcement action.

For directors facing HMRC pressure, it’s important to understand that continuing to trade while knowingly insolvent can lead to personal liability for company debts. This makes seeking professional advice crucial as soon as tax payment problems arise.

How Anderson Brookes Can Help

At Anderson Brookes, we specialise in helping directors navigate the complex process of closing companies with HMRC tax debts. Our experienced insolvency practitioners provide comprehensive support throughout the closure process. This form part of our company debt solutions service.

We begin with a thorough assessment of your company’s financial position, including a detailed review of all HMRC liabilities across VAT, PAYE, Corporation Tax and any other tax obligations.

Our team can negotiate with HMRC on your behalf, potentially securing Time to Pay arrangements if your company has viable prospects for recovery and tax debt settlement.

If liquidation is necessary, we handle the entire CVL process from initial documentation to creditor communications and final dissolution, ensuring all statutory requirements are met.

Throughout the process, we provide clear guidance on director responsibilities and obligations to help protect you from personal liability risks associated with company closure.

Many directors don’t realise they may be entitled to redundancy payments when their company enters liquidation. Our team can assist with these claims, which can provide valuable financial support during this challenging transition.

FAQs

Can I close a limited company with HMRC debt by striking it off?

If HMRC is owed money, a strike off application is likely to be challenged. Where the company cannot pay, a formal procedure such as a CVL is often the most appropriate way to close the company and deal with creditors properly.

What if HMRC is the only creditor?

Even if HMRC is the only creditor, the company still has an outstanding liability. The right route depends on whether the company can repay. If it cannot, a CVL may still be appropriate.

What if the company can repay but needs time?

If the company is viable and the issue is cashflow, a Time to Pay arrangement may be suitable. If the company has several creditors and needs a structured repayment plan, a CVA may be worth exploring.

Can HMRC take action if I do nothing?

HMRC has a range of recovery powers and will often escalate if arrears remain unpaid. If you can’t repay, the earlier you deal with it properly, the more control you usually keep over the outcome.

Can I start a new company after closing one with HMRC debt?

In many cases, directors can continue to trade in the future, but it depends on the circumstances and how the closure is handled. The safest approach is to take advice early and follow the correct process.

How long does it take to close a limited company through CVL?

Timescales vary depending on the complexity of the company, the level of creditor activity, and whether assets need to be realised. We can give a clearer indication once we understand the facts of your case.

Will I be personally liable for HMRC debt?

Company debts are generally company liabilities, but there are situations where personal exposure can arise. It depends on what has happened within the company, whether there are personal guarantees, and how matters are handled once insolvency is likely.

Speak to Anderson Brookes

If you’re dealing with HMRC debt and need to close a limited company, Anderson Brookes can help you understand the right route and the next steps. We’ll talk you through the options and explain the implications clearly so you can make a decision with confidence.

To get in contact, call 0800 1804 935, email advice@andersonbrookes.co.uk or use our contact form.